Affine Point Processes: Approximation and Efficient Simulation

Abstract

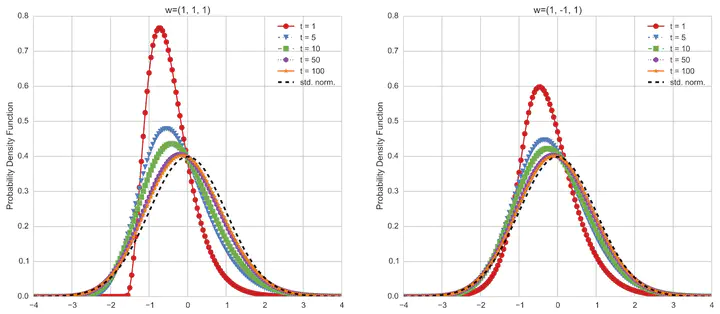

We establish a central limit theorem and a large deviations principle for affine point processes, which are stochastic models of correlated event timing widely used in finance and economics. These limit results generate closed-form approximations to the distribution of an affine point process. They also facilitate the construction of an asymptotically optimal importance sampling estimator of tail probabilities. Numerical tests illustrate our results.

Type

Publication

Mathematics of Operations Research 40(4):797–819

Xiaowei Zhang

Associate Professor

My research research focuses on methodological advances in stochastic simulation and optimization, decision analytics, and reinforcement learning, with applications in service operations management, FinTech, and digital economy.