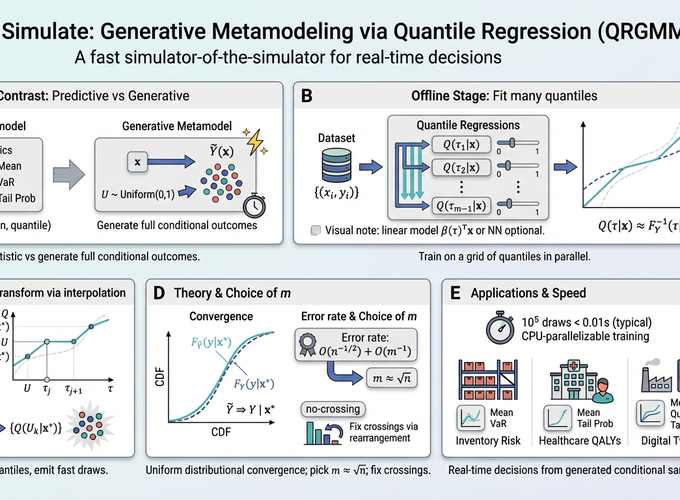

Stochastic simulation models effectively capture complex system dynamics but are often too slow for real-time decision-making. Traditional metamodeling techniques learn relationships between simulator inputs and a single output summary statistic, such as the mean or median. These techniques enable real-time predictions without additional simulations. However, they require prior selection of one appropriate output summary statistic, limiting their flexibility in practical applications. We propose a new concept: generative metamodeling. It aims to construct a ‘‘fast simulator of the simulator,’’ generating random outputs significantly faster than the original simulator while preserving approximately equal conditional distributions. Generative metamodels enable rapid generation of numerous random outputs upon input specification, facilitating immediate computation of any summary statistic for real-time decision-making. We introduce a new algorithm, quantile-regression-based generative metamodeling (QRGMM), and establish its distributional convergence and convergence rate. Extensive numerical experiments demonstrate QRGMM’s efficacy compared to other state-of-the-art generative algorithms in practical real-time decision-making scenarios.