Smooth Nested Simulation: Bridging Cubic and Square Root Convergence Rates in High Dimensions

Abstract

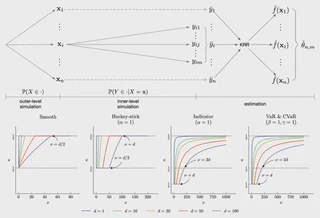

Nested simulation concerns estimating functionals of a conditional expectation via simulation. In this paper, we propose a new method based on kernel ridge regression to exploit the smoothness of the conditional expectation as a function of the multidimensional conditioning variable. Asymptotic analysis shows that the proposed method can effectively alleviate the curse of dimensionality on the convergence rate as the simulation budget increases, provided that the conditional expectation is sufficiently smooth. The smoothness bridges the gap between the cubic root convergence rate (that is, the optimal rate for the standard nested simulation) and the square root convergence rate (that is, the canonical rate for the standard Monte Carlo simulation). We demonstrate the performance of the proposed method via numerical examples from portfolio risk management and input uncertainty quantification.

Type

Publication

Management Science 70(12):9031-9057

Authors

Presidential Young Professor in the Department of Industrial Systems Engineering and Management, National University of Singapore.

Authors

PhD student in the Department of Industrial Engineering and Decision Analytics, HKUST.

Authors

I am an Associate Professor at HKUST, jointly appointed in the Department of Industrial Engineering and Decision Analytics and the Department of Economics, and the Academic Director of the MSc in FinTech program. I serve as an Associate Editor for several leading journals in the field, including Management Science, Operations Research, Navel Research Logistics, and Queueing Systems.